Switzerland’s energy transition is increasingly being engineered around one fundamental premise: hydropower is no longer simply a low-carbon generation source, but the primary balancing mechanism underpinning national system reliability.

While solar PV is expected to dominate future capacity additions, Swiss policymakers and utilities are relying on alpine hydro reservoirs and pumped storage assets to absorb renewable intermittency, stabilise frequency excursions and mitigate winter supply deficits. The result is a structural repositioning of hydropower within the country’s electricity architecture.

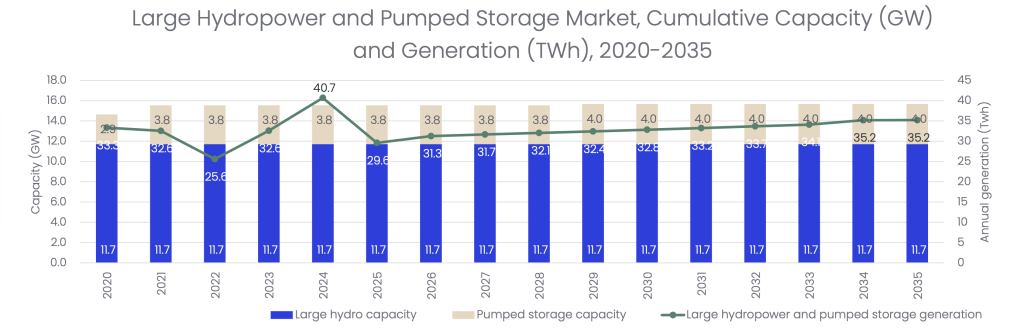

According to the latest Switzerland Power Outlook from Global Data, large hydropower and pumped storage represented 51.3% of installed capacity in 2025 and generated approximately 47.3% of total electricity output. Although solar capacity growth will progressively dilute hydro’s share of installed generation assets, hydroelectric infrastructure will remain indispensable to system operations through 2035 and beyond.

Pumped storage becomes a strategic balancing asset

The strategic significance of hydro has intensified following the Federal Act on a Secure Electricity Supply from Renewable Energy Sources, approved by Swiss voters in 2024. The legislation accelerated deployment targets for domestic renewables while explicitly prioritising winter adequacy, storage and grid resilience. Subsequent amendments to the Electricity Supply Act introduced a formal electricity reserve mechanism comprising hydropower reserves, thermal backup capacity and demand-side balancing resources.

For hydro operators, the implications are substantial. Flexibility and dispatchability are now valued as highly as energy production itself.

Switzerland’s large reservoir fleet gives the country a unique operational advantage within continental Europe. Unlike many neighbouring markets that are heavily exposed to short-duration battery systems or gas-fired balancing assets, Switzerland possesses long-duration hydro storage capable of seasonal energy shifting. This capability is becoming increasingly critical as solar generation penetrates deeper into the national supply mix.

Installed solar PV capacity accounted for 31.7% of total capacity in 2025 and is projected to dominate renewable investment through 2030, attracting more than 90% of total new-build investment allocation. Yet the operational challenge associated with this build-out is fundamentally seasonal. Swiss winter electricity demand coincides with declining solar irradiation, lower hydro inflows and elevated heating loads, increasing exposure to imports during periods of continental market stress.

Hydropower is therefore being repositioned as the principal instrument for managing seasonal volatility.

The expansion of pumped storage is central to this strategy. Nant de Drance, commissioned in 2022 with approximately 900MW of capacity and around 20GWh of storage, represents the clearest example of Switzerland’s transition toward flexibility-oriented hydro infrastructure. Additional decentralised pumped storage opportunities are also being evaluated under initiatives such as HiDeStor, reflecting growing interest in medium-scale storage systems integrated closer to regional load centres.

At the same time, existing hydroelectric assets are entering a new investment cycle focused on refurbishment, turbine modernisation and operational optimisation rather than conventional greenfield expansion. Switzerland’s large hydropower capacity is forecast to remain essentially flat at 11.7GW through 2035, indicating that future gains will come primarily from efficiency improvements, digital optimisation and enhanced storage utilisation rather than major new dam construction.

Flexibility markets reshape hydro operations

Generation performance, however, remains highly hydrology-dependent. Output from large hydro and pumped storage fell from 40.7TWh in 2024 to 29.6TWh in 2025 before recovering toward 35.2TWh by 2035. This volatility is reinforcing the need for more sophisticated reservoir management strategies, probabilistic inflow forecasting and expanded ancillary services participation.

Swissgrid’s evolving balancing framework is likely to accelerate this transition further. As renewable intermittency increases, balancing markets are becoming more granular and increasingly accessible to distributed flexibility providers. Hydropower operators are consequently adapting assets for faster ramping capability, more dynamic dispatch cycles and participation across multiple market layers including intraday trading, frequency containment reserve and tertiary balancing services.

Digitalisation is becoming equally important. The nationwide rollout of smart metering infrastructure and advanced demand-response mechanisms is expected to reshape load behaviour and create more responsive balancing ecosystems. For hydro operators, this creates opportunities to monetise flexibility in ways that were previously unavailable within Switzerland’s relatively conservative market structure.

Nevertheless, significant structural constraints remain. Permitting complexity continues to slow hydro development, particularly in environmentally sensitive alpine regions where projects can spend more than a decade navigating federal, cantonal and municipal approval processes. Public opposition to landscape impacts, ecological concerns and transmission expansion remains a recurring challenge even as national political support for energy security strengthens.

Grid constraints are also becoming increasingly material. Distribution infrastructure in several regions is already struggling to accommodate reverse power flows associated with high solar penetration, creating operational bottlenecks that ultimately increase reliance on flexible hydro dispatch.

Against this backdrop, Switzerland’s hydro sector is evolving from a mature conventional generation industry into a high-value flexibility business. That evolution will define the next decade of Swiss power engineering. While solar PV may dominate future capacity statistics, hydroelectric infrastructure will remain the operational core of the system, balancing renewable variability, preserving winter adequacy and anchoring Switzerland’s role within the broader European electricity market.

In practical terms, the country’s decarbonisation pathway increasingly depends not on how much hydropower Switzerland builds, but on how intelligently and flexibly it operates the hydro assets it already possesses.